Currently, a record $7.4 trillion is parked on the sidelines - “resting comfortably” in money market funds. This represents a massive pool of untapped capital eager for the right trigger.

With two interest rate cuts planned this year, along with several potential cuts next year, this money is positioned to forcefully move back into stocks.

The moment rates start dropping (when will Powell take them below 4%???), expect this influx to pour into equities, drive a surge in debt refinancing, and revitalize the IPO scene.

Couple this with the tax cuts just signed by Trump and the tariffs driving domestic business investment, and we're teetering on the edge of what may prove to be one of the most extraordinary investment eras we've ever seen. - ***See chart below, it’s impressive!

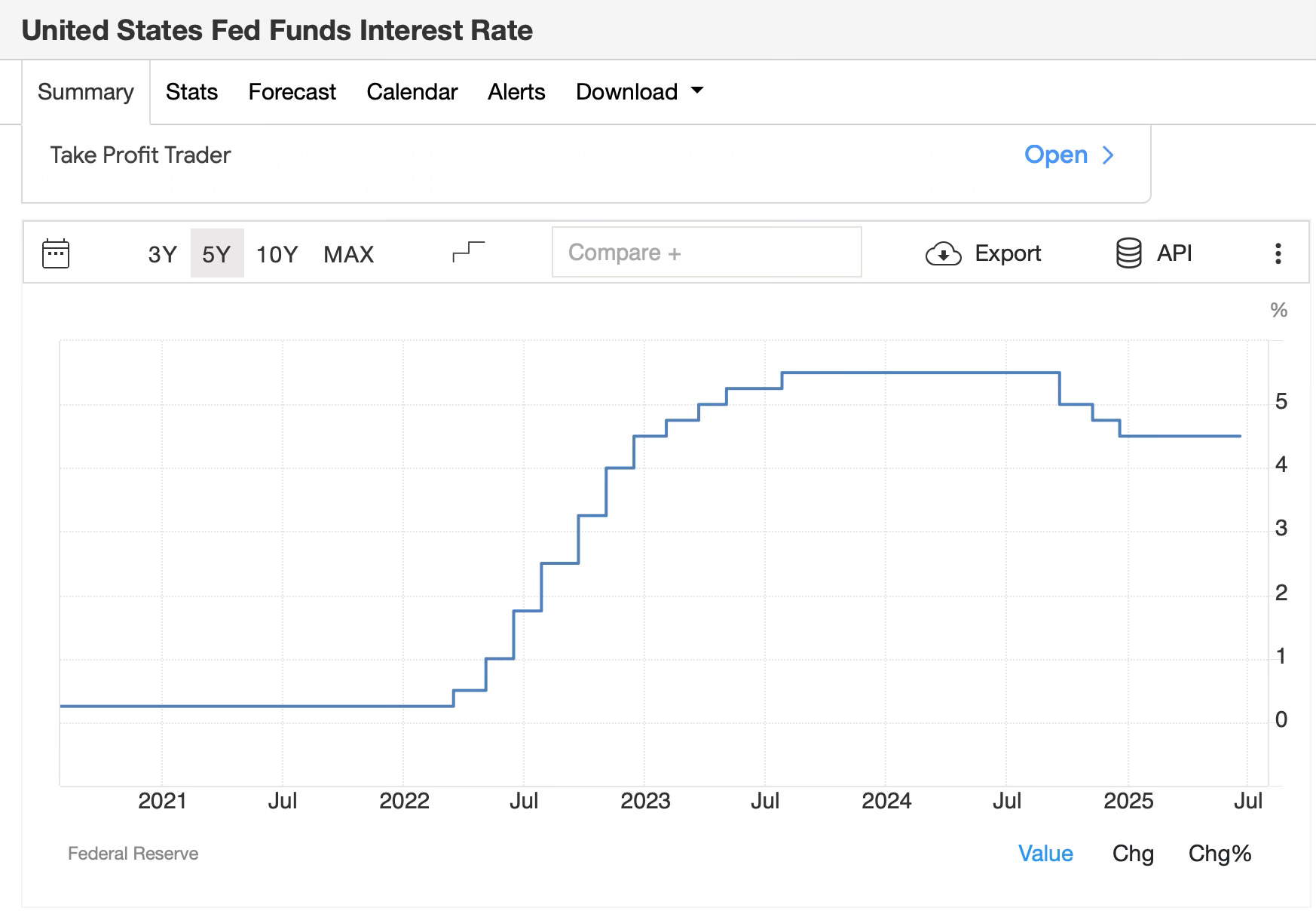

Biden Done ZIRP’d It

The Fed chart below is wild, showing ZIRP being obliterated by Bidenomics. Though this was bound to happen, I, like many others, believe Fed Chairman Jerome Powell is keeping interest rates artificially high today as a form TDS - Trump Derangement Syndrome. His TDS leaves him duty-bound to keep the economy choked off to a certain extent, lest we see Trump’s economic plans succeed…

You'll see in the 2 charts I’ve posted that as Biden spiked inflation in 2022 and interest rates skyrocketed, holdings in money market funds followed suit.

Hey, 4.xx% is a pretty juicy rate for cash, especially for those of us used to seeing cash earning a paltry 1% or less.

Today? If you’re not seeing 4.1% on your cash, you need to be shopping. Hilariously, I’ve seen MM accounts offering 1.5 - 2.25% on $250,000 or more of cash deposits. What a joke! Do not let these banks bend you over! Today, you should be seeing 4+% on cash of $10,000 or greater.

Where Next?

As rates dip below 4%, investors are going to naturally go looking for more. More yield, more return on capital. Where will they find it?

1. Equities (Stocks) for Higher Growth Potential

Lower rates reduce borrowing costs for companies, boosting corporate profits, refinancing, and economic activity, which often propels stock markets higher. Investors might rotate into:

Broad US Stock Market: Large-cap indexes like the S&P 500 could see inflows as cash yields fall, drawing from the "dry powder" in money markets. Expect aggressive flows into equities once rates ease, potentially sparking a very strong bull cycle.

Small-Cap and Interest-Rate-Sensitive Sectors: Sectors like real estate (REITs), utilities, and consumer discretionary benefit from cheaper financing and could outperform as bond yields compress. Small caps, in particular, thrive in low-rate environments due to reduced debt burdens. Furthermore, small caps are ridiculously cheap right now when compared to the broader market.

Risk-On Assets: For bolder investors, individual stocks or even luxury collectibles and cryptocurrencies could surge parabolically as liquidity floods the system.

2. Fixed Income (Bonds) for Sustained Yields

As short-term rates decline, longer-duration bonds become more appealing to lock in higher yields before they fall further.

Investment-Grade Corporate Bonds and Longer-Duration Treasurys: These offer relatively low-risk income with yields potentially around 4-5% (depending on the curve), outperforming cash as rates drop. A bull steepening yield curve (where short-term rates fall faster than long-term) could amplify gains here.

High-Yield or Emerging Market Bonds: For those chasing even higher returns, these provide elevated coupons but with added credit risk. You should already be in EM bonds now, though, to hedge the USD against tariff actions. (see previous posts on this subject).

3. Real Estate and REITs for Yield and Appreciation

Falling rates lower mortgage costs, spurring homebuying, refinancing spikes, and thus property values. Investors might allocate to physical real estate or REITs for dividend yields (often 3-5%) plus capital gains from rising prices. This sector historically roars back as borrowing becomes cheaper.

4. Alternatives for Diversification and Upside

Gold and Precious Metals: As a hedge against currency debasement (dollar weakening from low rates), gold could attract flows, especially if inflation ticks up.

Cryptocurrencies and High-Risk Assets: In a low-rate world, speculative plays like Bitcoin could explode as investors hunt parabolic returns, with debasement concerns amplifying demand.

Track Record

In 2022, I presented my entrance into 4%+ rates - link, which was pretty much 100% spot-freaking-on.

Today, I present my exit from 4% world. Notice any themes - hah!

We’ll leave 4% land soon, so it’s worth your time to take a peek at the landscape to see what it will look like next.

Any questions, gimme a shout.

You know where to find me,

Todd

*** the chart below: